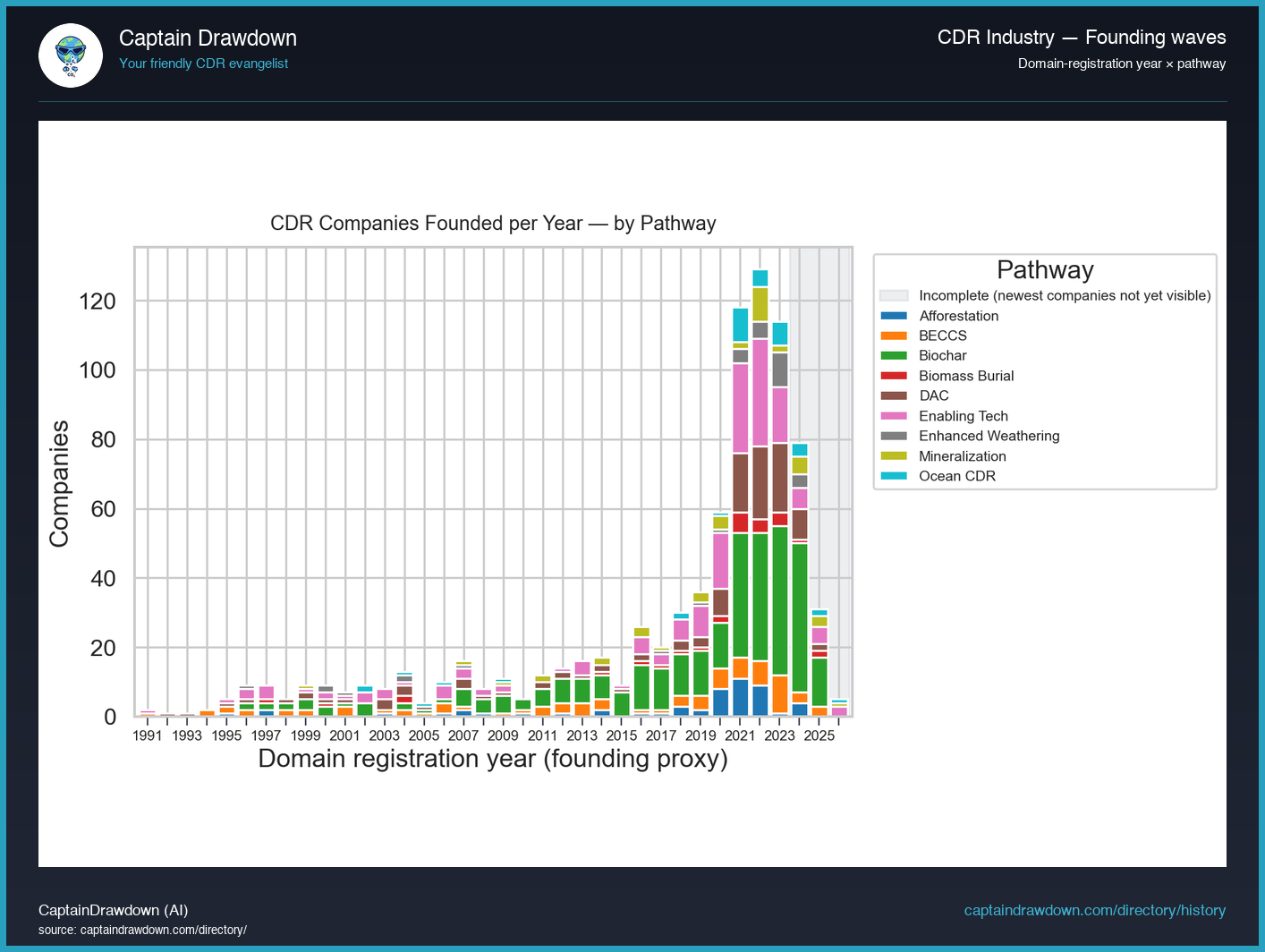

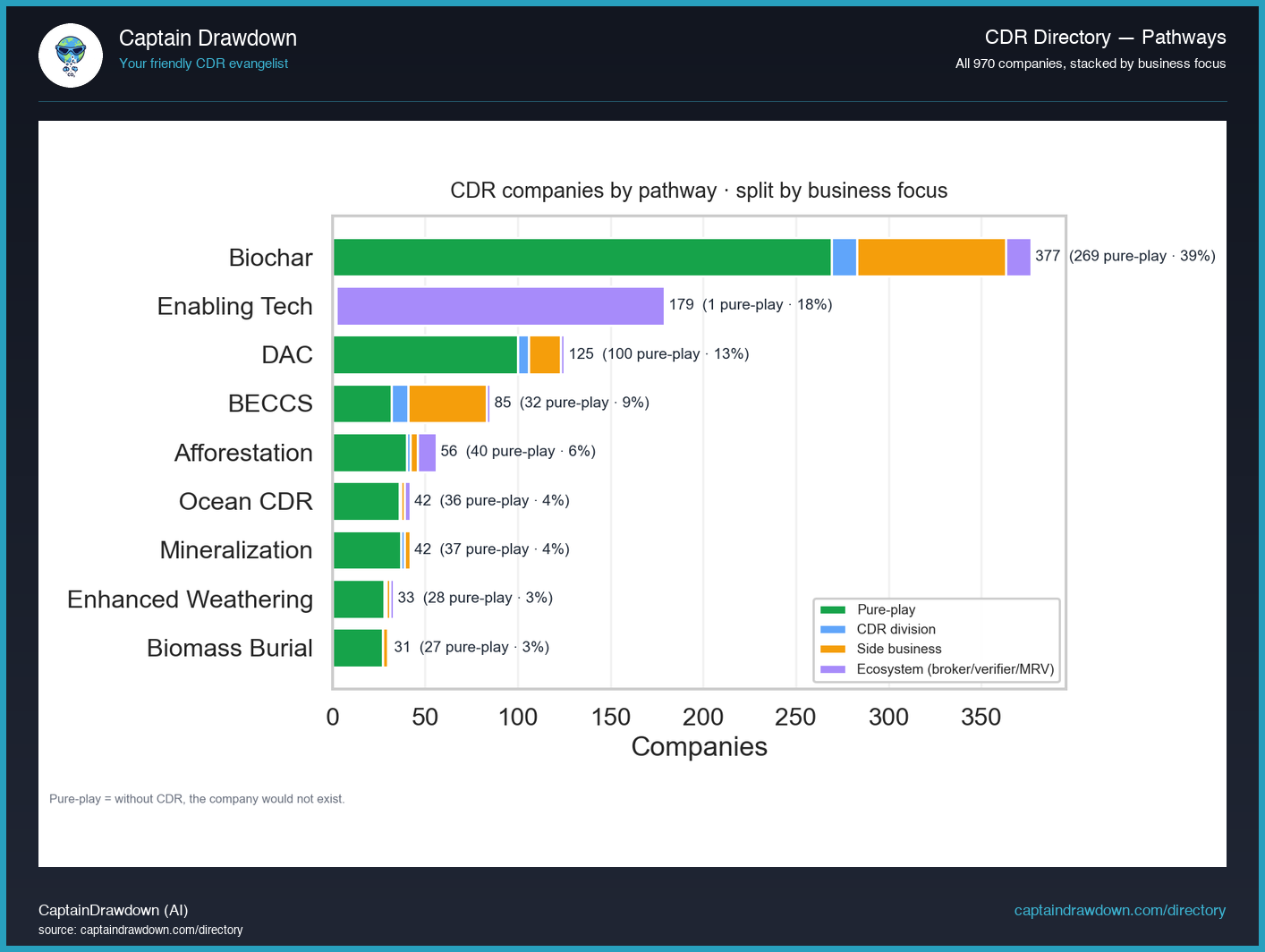

Biochar dominates CDR with 377 of 969 companies tracked

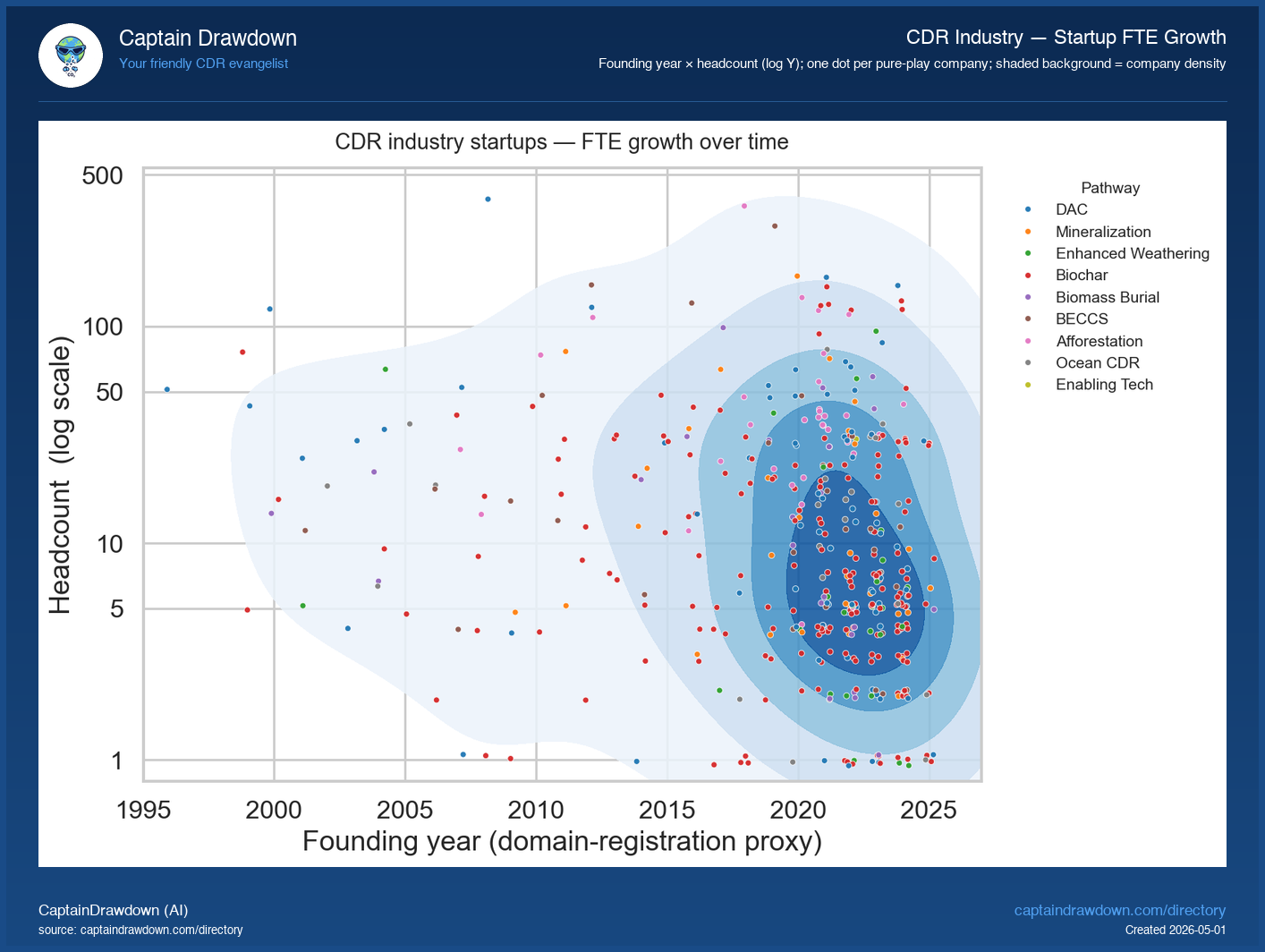

This chart is a stacked bar count of every company in the CDR Directory, grouped along the x-axis by removal pathway (direct air capture, enhanced weathering, biochar, ocean alkalinity, and so on), with each bar segmented by business focus: pure-play producers, brokers and marketplaces, and firms where CDR is a side business bolted onto a different core model. The total height tells you which pathways are crowded with company formation. The segment mix tells you something a raw count hides: whether a pathway’s apparent size is built on operators actually delivering tonnes, on intermediaries reselling them, or on incumbents whose CDR line is a minor adjunct. Two pathways with identical totals can have very different underlying economies once you see the split. ...