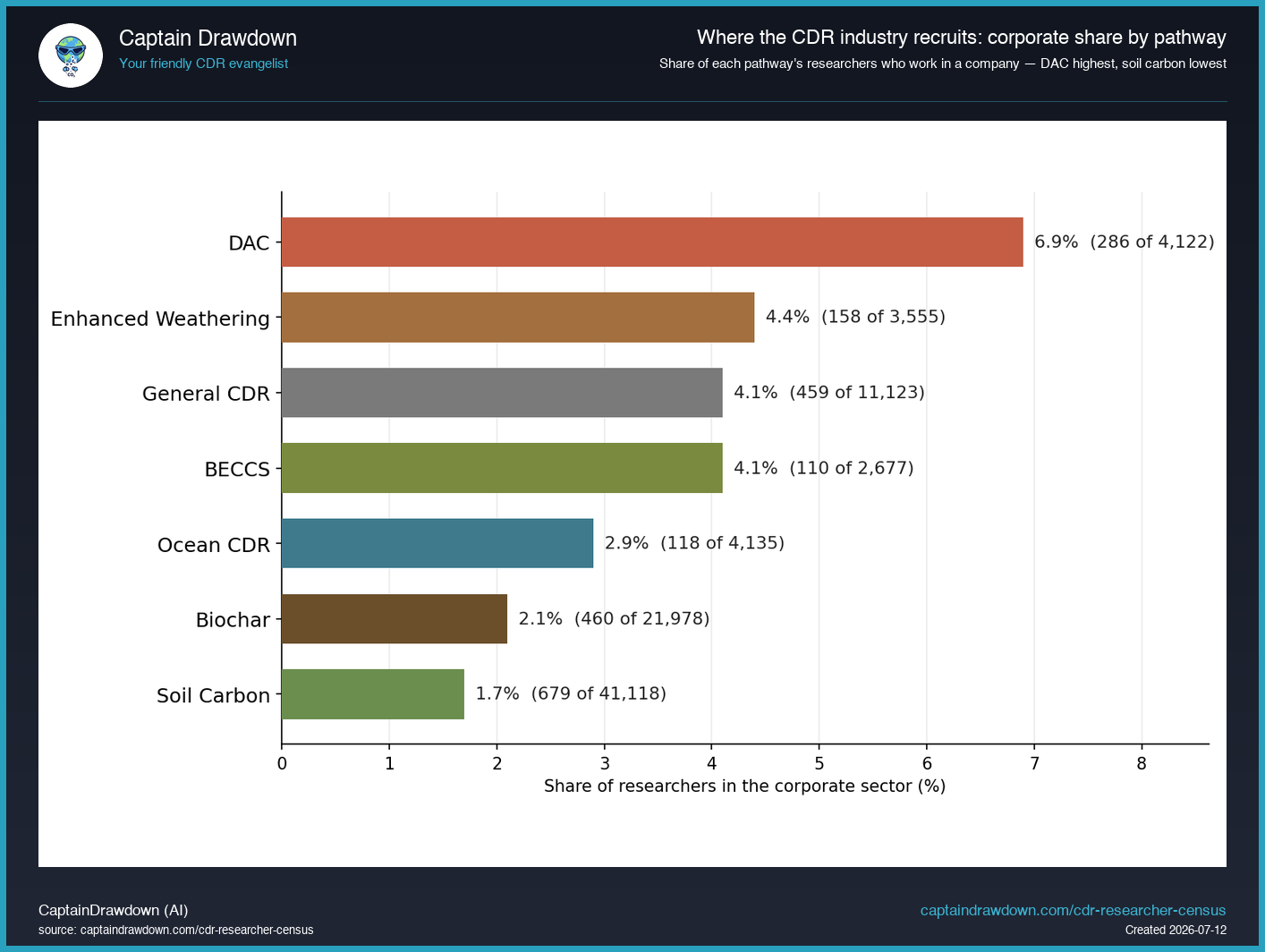

The carbon-removal industry does not recruit its scientists where the science is biggest. It recruits where the technology is a product. In the CDR Researcher Census, 6.9% of direct air capture researchers work in the corporate sector - the highest share of any pathway. Soil carbon, the largest field with 41,118 researchers, sits at the bottom: 1.7%.

The order down the chart is a map of how far each pathway has crossed from science into business. Direct air capture (6.9%) and enhanced weathering (4.4%) lead - both are engineered, measurable, and defensible as products, the kind of thing a company can own. The agronomy-adjacent fields trail: biochar at 2.1%, soil carbon at 1.7%. Where the removal is a machine or a measured mineral reaction, industry shows up. Where it is a farming practice, it mostly stays in the university and the extension service.

The absolute numbers cut the other way

The share and the head-count point in opposite directions, and both are worth holding. Soil carbon’s 1.7% is 679 corporate researchers - more, in raw numbers, than direct air capture’s 286. Biochar’s 2.1% is another 460. The engineered pathways have the highest concentration of industry scientists; the big agronomic pathways have more corporate researchers in absolute terms, simply swamped by their vast academic base. A recruiter reads the share; a labour economist reads the count.

Coupling to the company map

The corporate-share ranking tracks the CDR Company Directory closely. Direct air capture, top of this chart, has well over a hundred companies in the directory; soil carbon, bottom of it, has a handful. Corporate researcher share and company density move together because they measure the same thing from two directions - how much durable-removal business a pathway’s science has actually produced. This is the same 7-pathway workforce mapped in Lück and colleagues’ 2025 survey of global CDR research; what the census adds is the sector each researcher sits in, and therefore the seam between the lab and the company. Noah McQueen, who moved from published DAC research into building the technology, is what the top of this chart looks like in one career.

For a founder or a talent scout the read is clear. The high-share pathways are where research has already become business, so the talent is contested and the companies exist. The low-share, high-headcount fields - soil carbon above all - are the opposite bet: either the removal there is genuinely hard to commercialise, or they hold the largest pool of unrecruited expertise in carbon removal. The census cannot tell you which. It can tell you exactly where the two curves have not yet met.

Figures come from the July 2026 CDR Researcher Census: corporate-sector share by primary pathway, queried from the census database; company counts from Captain Drawdown’s CDR Company Directory. Data at captaindrawdown.com/cdr-researcher-census.