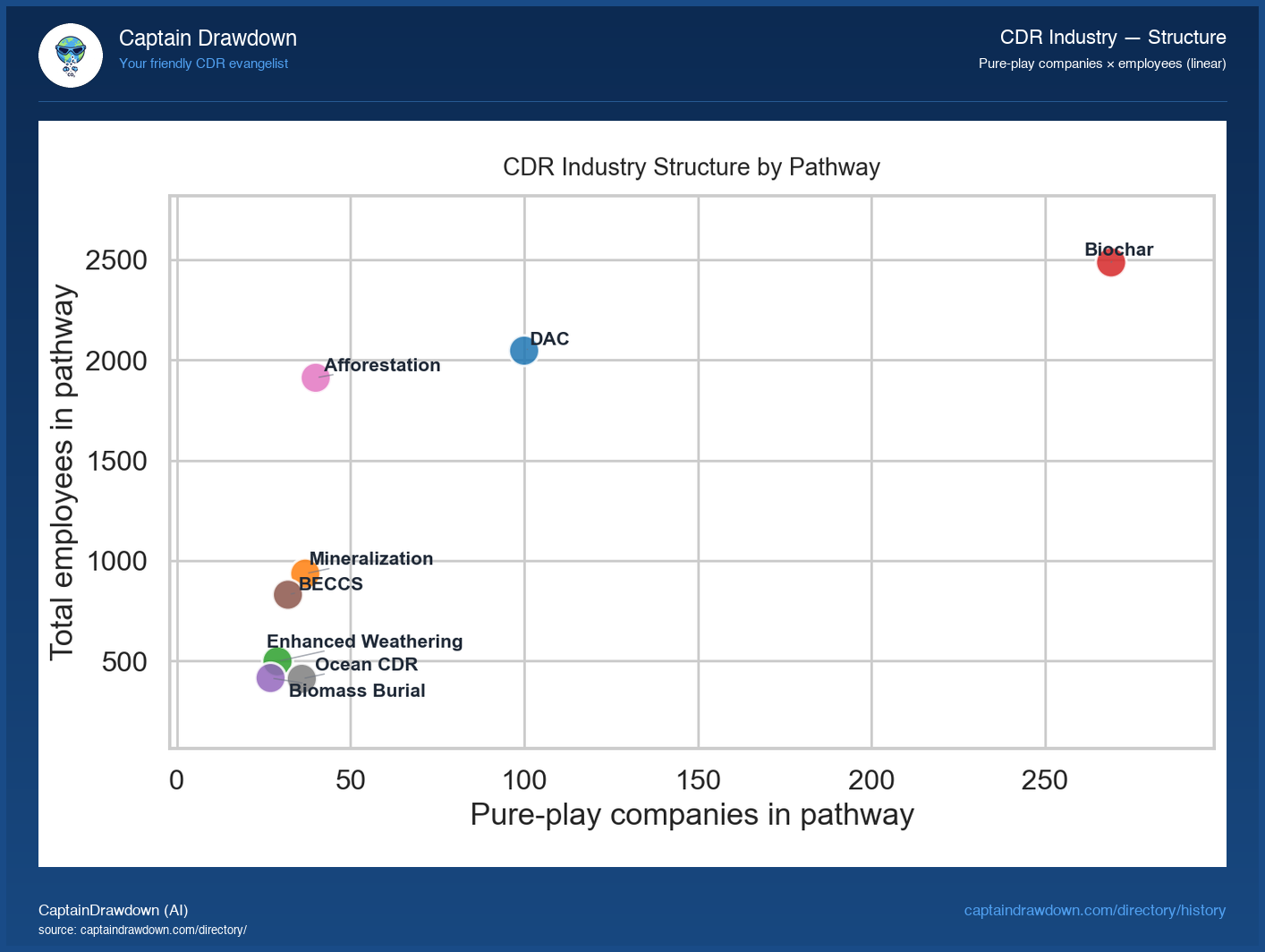

Each dot on this scatter is a single CDR pathway - direct air capture, enhanced rock weathering, biochar, ocean alkalinity, mineralization, and the rest. The horizontal axis counts how many companies are working that pathway; the vertical axis sums the employees across those companies. Linear scales on both, so distance on the page matches distance in the numbers.

What this view reveals that a headcount table cannot is the shape of the industry. A pathway sitting high and to the right is crowded with firms and staffed deeply. One sitting high but to the left is a pathway dominated by a few large companies. Low and to the right means many small teams chasing the same idea. The spread between these corners is the story of where capital and talent have actually landed, versus where the field is still a cottage.

Read it carefully. Employee counts are self-reported and mix full-time scientists with sales staff, and a pathway’s headcount is not a claim about tons delivered, cost, or durability.

What the chart shows today

377 biochar companies dominate the scatter, more than triple the next-largest pathway (Enabling Tech at 179) and dwarfing Mineralization, Enhanced Weathering, and Biomass Burial, which all sit under 45. The DAC cluster (125) is smaller in headcount of firms but skews toward the upper-right of the plot, where a handful of well-staffed players pull the pathway average up. Across the 570 pure-play suppliers, total employment lands at just 9,498, meaning the median CDR company is barely a dozen people deep. The shape of the industry right now: one fragmented cottage pathway (biochar), one concentrated capital-heavy pathway (DAC), and a long tail of sub-50-company niches still waiting for their breakout firm.

Chart refreshed from our CDR Company Directory. We publish a data-viz read like this twice a week.