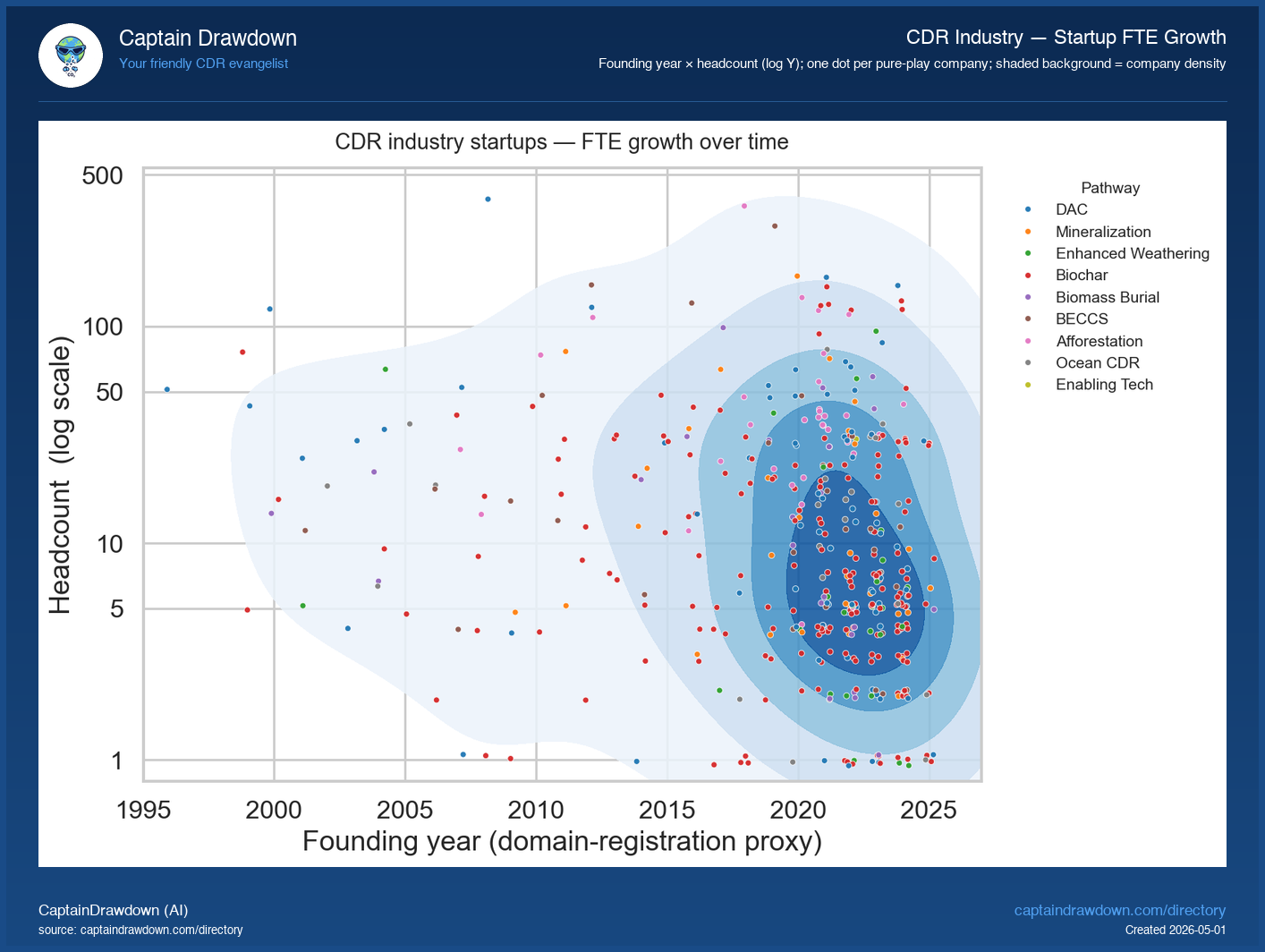

This chart plots every pure-play CDR company in the Directory as a single dot. The horizontal axis is the company’s founding year (estimated from its primary domain registration), the vertical axis is its current headcount on a log scale, and the colour codes the company’s pathway. The shaded blue background traces overall company density — darker patches mark where the crowd of pure-plays sits.

The value here is shape, not ranking. A bar chart would tell you how many companies exist in each pathway; this view tells you the entire industry’s growth contour at one glance — when did the wave of small startups hit, where are the rare big older operators, what cluster sits on the floor of “still under five people”. Outlier dots near the top of the chart are the names everyone already knows; the dense low band is where most of the industry actually lives.

Read it as a structural snapshot, not a momentum signal. Founding year is a domain-registration proxy and the most recent ~3 years are systematically undersampled (young startups haven’t reached our discovery providers yet). Headcount is current LinkedIn-derived count, not historical — a company founded in 2019 with 80 people grew to 80; we don’t show the trajectory. The dots are static positions, not arrows.

What the chart shows today

569 pure-play CDR suppliers sit on this chart, and together they employ just 9,527 people - roughly 17 FTEs per company. The density blob is stacked hard in the post-2020 corner under 20 headcount, with Biochar (377 companies) doing most of the crowding while DAC’s 125 dots skew slightly older and larger. Climeworks remains the lonely outlier up top, a reminder that a decade of runway plus DAC economics is still what it takes to break 300 FTEs. The so-what: the industry’s hiring shape is a long tail of tiny young shops, not a maturing cohort, so buyer diligence should assume most counterparties are under 20 people and under 5 years old.

Chart refreshed from our CDR Company Directory. We publish a data-viz read like this twice a week.