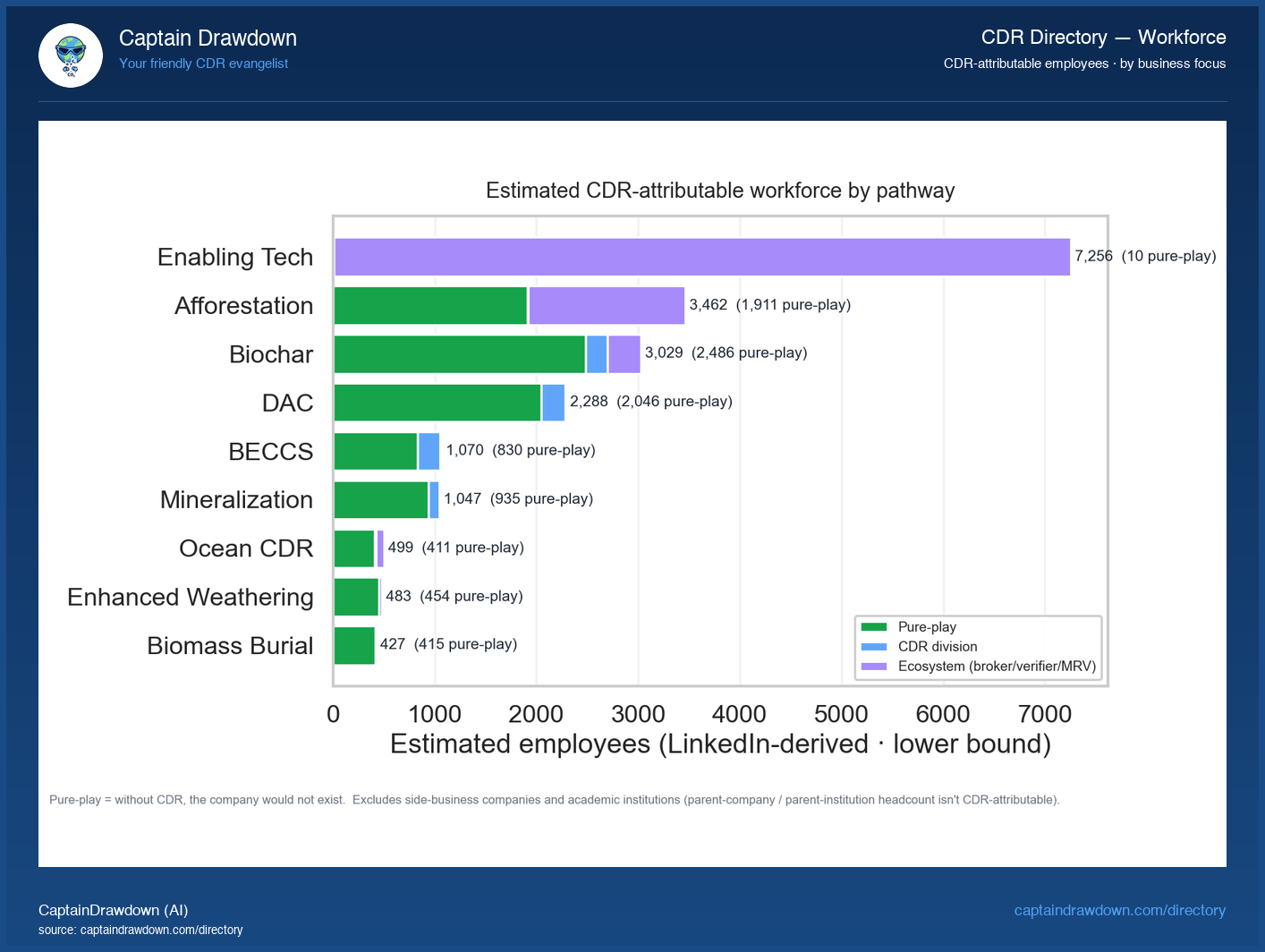

This chart is a stacked horizontal bar showing CDR-attributable headcount across pathways on the vertical axis, with each bar segmented by business focus: pure-play companies whose entire reason for existing is CDR, divisions inside larger firms where CDR is one line of business, and ecosystem players who sell tools, verification, brokerage, or software into the space. Bar length is total attributed workers; the color split is where those workers actually sit.

The useful pattern here is the ratio, not the totals. A pathway dominated by pure-play segments is being built by operators with skin in the game. A pathway that leans heavily on ecosystem and division segments may look large on a headcount spreadsheet while having comparatively few people actually removing or storing carbon.

Read it carefully. Headcount is not tonnage, not revenue, and not durability. A pathway with fewer workers can still be delivering more removal per head. Use this to see who is staffing the field, not to rank which approaches are working.

What the chart shows today

Biochar leads the field with 377 companies, more than DAC (125) and BECCS (84) combined, while Enabling Tech sits second at 179 - meaning roughly one in five entries in the directory builds tools for removal rather than doing it. Of the 969 companies visible, 569 are pure-play CDR businesses employing 9,527 people, which averages out to fewer than 17 employees per company. The rest of the field splits into 211 ecosystem players, 154 side businesses, and just 35 corporate divisions. The takeaway: the CDR workforce is dominated by small, dedicated shops rather than big-company divisions, so headline job numbers here reflect hundreds of startups still years from scale, not an established industry.

Chart refreshed from our CDR Company Directory. We publish a data-viz read like this twice a week.