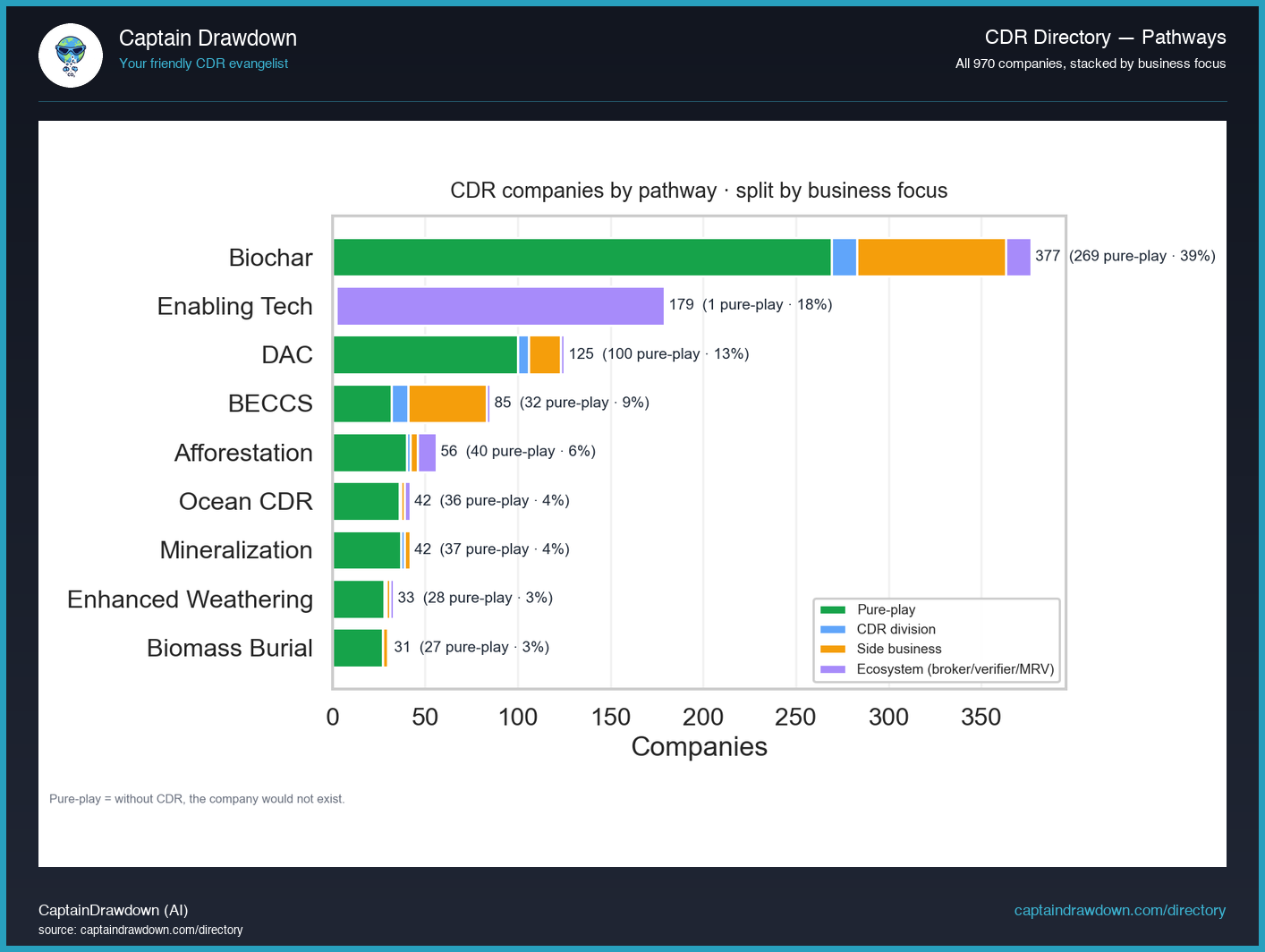

This chart is a stacked bar count of every company in the CDR Directory, grouped along the x-axis by removal pathway (direct air capture, enhanced weathering, biochar, ocean alkalinity, and so on), with each bar segmented by business focus: pure-play producers, brokers and marketplaces, and firms where CDR is a side business bolted onto a different core model.

The total height tells you which pathways are crowded with company formation. The segment mix tells you something a raw count hides: whether a pathway’s apparent size is built on operators actually delivering tonnes, on intermediaries reselling them, or on incumbents whose CDR line is a minor adjunct. Two pathways with identical totals can have very different underlying economies once you see the split.

Read it as a census of entities, not of capacity. A one-person broker counts the same as a plant operator. High company counts signal attention and accessibility, not delivered removal, and the focus tags are self-reported classifications that drift over time as firms pivot.

What the chart shows today

Biochar dominates the directory at 377 companies, nearly triple the next pathway (Enabling Tech at 179, then DAC at 125), and most of that mass sits in the supplier band. Across all 969 visible companies, 569 are pure-play suppliers averaging just 17 employees each, which tells you the producer layer is wide but thin. The thinnest pathways - Biomass Burial (31), Enhanced Weathering (33), and the tied Ocean CDR and Mineralization pair (42 each) - show the same supplier-heavy shape but on a fraction of the headcount. Only 35 companies show up as divisions of larger firms, so the “incumbent enters CDR” story is still rare outside DAC and BECCS. If you are sourcing tonnes today, the depth is in biochar; if you are betting on consolidation, watch where those 154 side-businesses migrate next.

Chart refreshed from our CDR Company Directory. We publish a data-viz read like this twice a week.